Fintech has moved from a category of products to the operating system of the financial services industry, with mobile-first delivery and API rails reshaping how customers reach financial products. The primary growth constraint has become engineering capacity in scarce specializations like security, compliance automation, and machine learning. This guide explains why talent strategy now determines who pulls ahead in fintech.

Key Points

- 1.4 billion adults remain unbanked (World Bank), and mobile-money accounts crossed 2 billion globally in 2024, which is where fintech growth still has the most headroom.

- 74% of employers globally report difficulty finding skilled engineering talent, which is the practical limit on how fast fintech companies can ship.

- Established banks have reorganized to ship like technology companies, using integrated partner models for digital lending and core modernization work.

- Engineering capacity is the most critical constraint on fintech growth, with regulatory and security skills the scarcest of all.

Over the past 15 years, financial technology has shifted from back-office plumbing to the operating system of the financial services industry. What began as upgrades to banking infrastructure now spans API-first platforms, embedded finance, and mobile-first products that support digital banking, financial planning, and automated financial advice.

This guide follows the broader arc: how fintech evolved from institutional enhancement to disintermediation; why its global spread rides on financial inclusion; and why engineering capacity, often via nearshore and offshore partnerships, now decides who ships, who complies, and who pulls ahead.

From Institutional Tool to Bank Disintermediation

ATMs and electronic trading were early forms of financial technology woven into legacy systems. The post-2008 period accelerated something different: a wave of fintech companies that rebuilt core banking services for the mobile era, payments, lending, and wealth, often without a traditional bank front and center.

Hallmarks of that phase

- Direct-to-consumer platforms in payments, credit, and investing reset acquisition economics and service models.

- Banking-as-a-Service and API rails let startups provision cards, accounts, and payments over compliant infrastructure, speeding time-to-market.

- Mobile-first delivery made banking feel like any other app: fast, context-aware, and available at the point of need.

The result was cultural as much as technical. Fintech firms are optimized for iteration and user experience; traditional financial institutions are optimized for stability and regulatory compliance.

Global Expansion and the Inclusion Imperative

The financial industry’s most dramatic fintech stories are in markets where traditional banks have thin coverage. In these regions, digital payment solutions and mobile wallets became the shortest route to inclusion, no branch build-out required.

The broader picture is bigger: in 2024, the world crossed 2 billion registered mobile-money accounts with over half a billion active monthly users. This is how far mobile wallets and agent networks have penetrated beyond the banking industry’s branch model.

Step back to the global view, and the job is unfinished. The World Bank’s Global Findex 2021 shows 1.4 billion adults remain unbanked, underscoring the headroom for financial inclusion through digital channels.

In Southeast Asia, Google-Temasek-Bain’s e-Conomy research tracks an internet economy that reached its $200 billion GMV milestone three years earlier than expected, a tailwind for financial services companies and platforms from wallets to online lending.

Fintech solutions win when they fit local behaviors and constraints, agent networks vs. branches, data-light apps vs. glossy dashboards, ID and fraud models tuned to the documents people actually have.

Why Software Talent Strategy Is Core to Scale

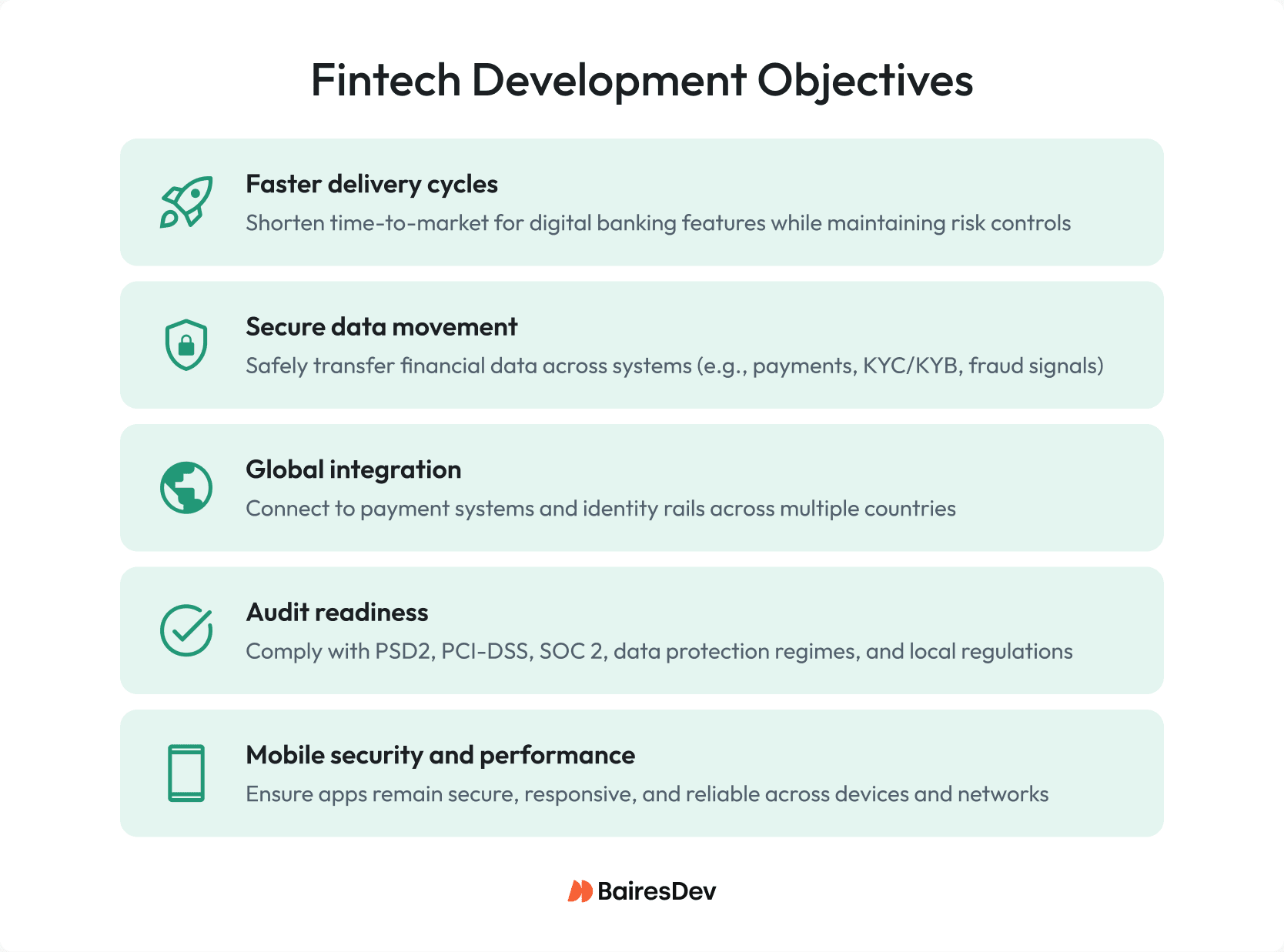

Fintech innovation is deeply tied to the ability to deliver complex, compliant, and secure software at speed. As competition intensifies, fintech companies are under pressure to deliver against aggressive growth and compliance objectives.

This takes scarce roles: mobile security, cloud reliability, data science for machine learning fraud models, cryptography for blockchain technology use-cases, and domain-literate QA. It’s not just a feeling, 74% of employers globally report difficulty finding the skilled talent they need, a shortage that is particularly acute in technology and engineering.

Outsourcing: A Strategic Imperative

Well-run nearshore/offshore partnerships help fintech businesses deliver financial services faster while maintaining standards:

- Burst capacity when a regulator deadline looms or a market launch is near.

- Specialist skills on tap: cryptography, smart contracts, algorithmic trading connectivity, observability, regulatory compliance automation.

- Local fluency to interpret rules (e.g., India’s e-KYC, Brazil’s open banking, Kenya’s mobile-money guardrails) and adapt product flows.

- Operational resilience by distributing work across delivery zones.

Partnerships that compress cycle time without expanding permanent headcount are a rational hedge.

Banks Are Following Suit

Established financial institutions are not sitting out. Large banks have reorganized to ship like technology companies: domain-based teams, product owners, and continuous delivery for regulated stacks.

Many have adopted integrated partner models across Eastern Europe, Latin America, and South/Southeast Asia to bring in technological expertise faster, particularly for digital lending, payment processing, portfolio management, and core-modernization work.

If a partner can harden your online banking stack, stabilize uptime on mobile banking apps, or accelerate an expense tracking module for SMEs, do it. The prize is measurable: lower incident rates, shorter release cycles, and audit readiness.

Regional Proximity as an Advantage

Nearshoring, working with teams in similar time zones, has matured into the default for cross-border collaboration that still feels “in-house.” For a US or Western European fintech company, that often means:

- Latin America for time-zone alignment and a deep bench in cloud and mobile, useful when payment apps and merchant onboarding need daily real-time collaboration.

- Eastern Europe for specialists in distributed ledger technology, cryptography, high-throughput systems, and capital markets connectivity.

- Southeast Asia for APAC rollouts and localization, where peer-to-peer payments and super-app ecosystems change the “normal” customer journey.

Beyond talent quantity, these regions bring context, what local regulators expect, which IDs are trusted, how consumers actually accept payments, and which communication channels convert. That matters when you need to provide financial services that feel native from day one.

Engineering Partnerships as Strategic Differentiators

The best engineering partners do more than add headcount, they reinforce architecture, DevSecOps, and delivery stability. With built-in redundancy and follow-the-sun support, they help protect critical transactions and maintain SLAs.

Their audit-tested processes support change management, access controls, and documentation. They scale flexibly around seasonality, launches, or new business models, and handle high-leverage functions like test automation, observability, and incident response. They act as an extension of your team: one backlog, shared metrics, clean code ownership, and a bias for observable systems. That’s how fintech stays fast and compliant.

What to Prioritize in the Next 12 Months

Keep the structure of your roadmap simple and outcome-tied.

Payments and onboarding where customers are

Ship improvements that remove friction from online banking and payment apps: stronger device binding, fewer steps for KYC, dynamic risk scoring using machine learning that reduces false positives. Measure drop-offs, authorization rates, fraud write-offs, and time-to-first-payment.

Data you trust, models you can explain

Centralize financial data with audit trails. Favor explainable models for credit and fraud over black-box scores where regulators expect reason codes. Keep humans in the loop on edge cases.

Compliance as product, not paperwork

Codify controls in pipelines (separation of duties, approvals, evidence). Automate artefact capture for PSD2, PCI-DSS, SOC 2. Treat regulatory compliance like an API dependency, versioned, tested, monitored.

Resilience before bells and whistles

Invest in observability, chaos drills, and incident response. Prove recovery time and data durability for regulators and enterprise customers. If you’re a business-to-business provider, your SLAs are your brand.

Talent pathways that scale

Blend FTE hiring, internal academies, and partner teams. Use nearshore hubs for day-to-day collaboration; reserve offshore for 24/7 operations and specialized builds.

Looking Ahead: Fintech Growth Depends on Global Talent Fluidity

As the fintech sector continues to grow, driven by embedded finance, digital identity, and real-time data infrastructure, engineering capacity will remain its most critical constraint. Fintechs must be prepared to scale quickly, operate securely, and deliver tailored experiences across fragmented regulatory landscapes.

This will not be solved through hiring alone, and the need for talented software developers will not diminish.

Conclusion

So, what is Fintech in 2026? It’s the practical integration of new technologies into the financial sector to provide services faster and more safely than legacy stacks allow.

If you lead in this space, whether at a fintech startup or an established financial institution, treat your talent strategy like infrastructure.

Pick partners who raise your bar, not just your headcount. Keep your focus on outcomes customers notice: faster onboarding, clearer fees, safer financial transactions, and tools that help real people manage personal finances and small-business cash flow.