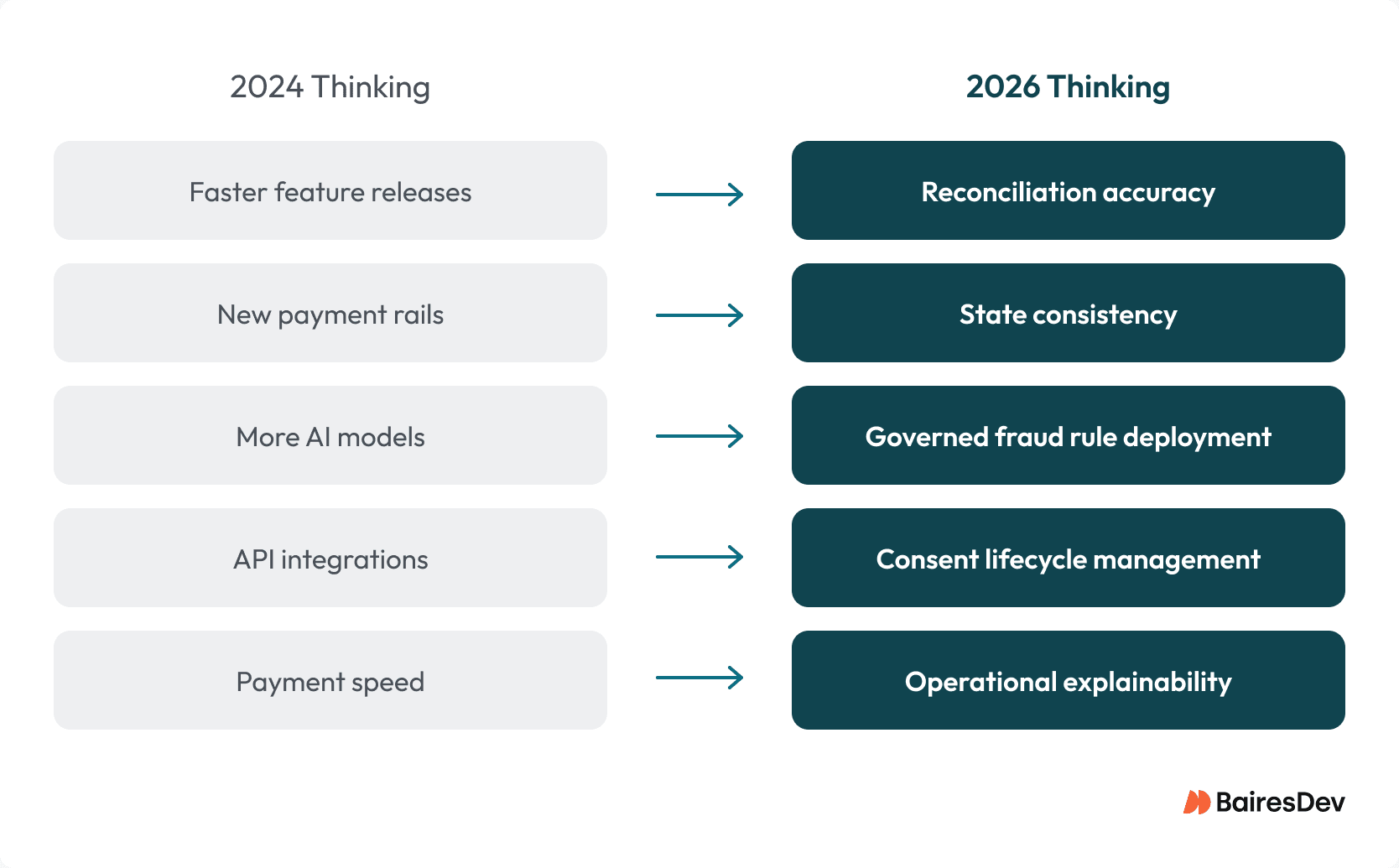

Fintech priorities in 2026 are shifting from feature delivery to operational resilience. Regulations including MiCA and PSD3, expanding real-time payment networks, richer payment standards such as ISO 20022, and increasingly sophisticated fraud attacks all require stronger platform controls rather than more product functionality.

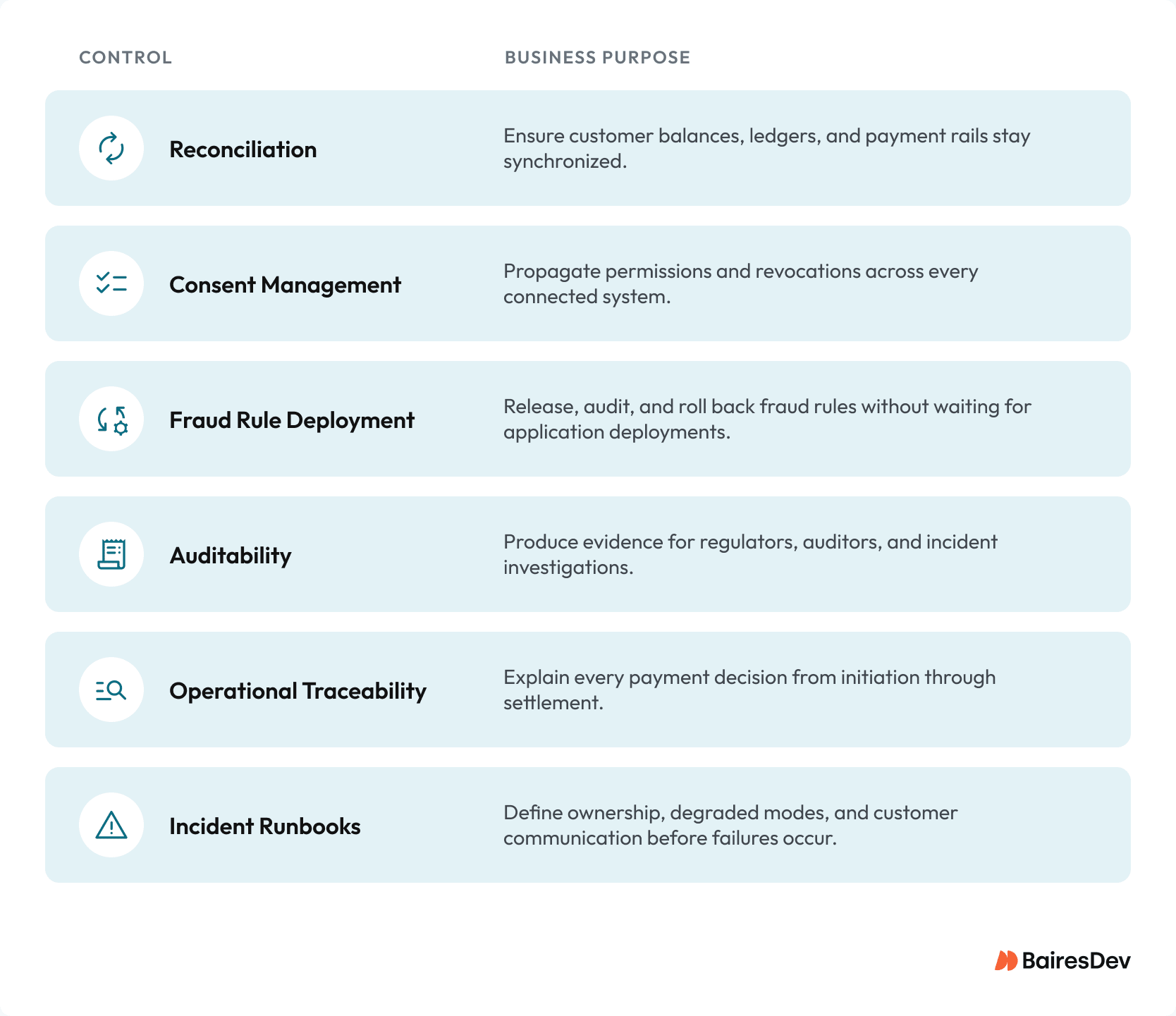

For engineering leaders, the highest-return investments sit in reconciliation, consent management, fraud rule deployment, auditability, and operational explainability, not in new payment rails or customer features. Organizations that strengthen these capabilities will be better positioned to scale products, satisfy regulators, and reduce operational risk.

Key Points

- Prioritize reconciliation before expanding payment rails.

- Make consent and entitlement first-class platform services.

- Treat fraud rules as software releases.

- Measure operational traceability.

Most fintech trend lists read like conference agendas: broad themes with little operational value. The shifts that matter in 2026 sit below the feature surface: in the operational controls, evidence trails, and operating models that determine whether a platform can survive scrutiny. They define who owns risk, how quickly systems must tell the truth, and where engineering leaders need to allocate capital before a roadmap turns into an incident review.

Across financial institutions and fintech companies, the center of gravity is moving from feature velocity to operational resilience. The future of fintech is being decided in reconciliation loops, consent systems, fraud rule pipelines, and support tooling. A platform can survive a missed feature window. It rarely survives a year of brittle payment infrastructure, weak fraud prevention, and financial transactions that appear settled before the books agree.

According to J.P. Morgan, over 70 countries have incorporated real‑time payment systems, with transaction volumes continuing to rise year over year. As instant settlement becomes standard across banking markets, customers increasingly expect balances, payment confirmations, and transaction status to agree across every channel and every moment of the payment journey. It’s a customer trust issue and, increasingly, a regulatory one.

Where Engineering Investment Is Moving in 2026

MiCA Turns Crypto Adjacency Into Infrastructure Work

For fintech companies that kept crypto at arm’s length, Europe’s Markets in Crypto‑Assets (MiCA) regulation shifts the posture from optional exploration to explicit regulatory framework. MiCA entered into force in 2023 and applied in phases, with stablecoin rules taking effect in mid-2024 and the full framework for crypto-asset service providers in December 2024, with the transition period for existing providers running through July 1, 2026. This introduced clearer rules around stablecoin issuance, custody, governance, and disclosure.

Europe isn’t the only jurisdiction raising the engineering bar. U.S. GENIUS Act and Hong Kong’s VASP licensing regime under its Anti-Money Laundering Ordinance point in the same direction: custody, governance, reserves, and auditability are becoming platform responsibilities rather than niche crypto concerns.

Legal teams feel this first, but it lands just as hard on financial infrastructure, release workflows, custody boundaries, and the systems that prove who approved what.

A team might want stablecoin support only for treasury or settlement use cases. Then it discovers that a reused fiat ledger no longer satisfies segregation requirements for financial assets. A release process that worked well for ordinary product changes fails once someone asks for durable evidence of dual approvals, break‑glass access, or reserve‑related controls.

Regulatory clarity narrows the room for “we’ll add the controls later.” That’s why MiCA belongs high on any 2026 list: it forces architectural decisions that crypto‑adjacent teams have deferred for years.

For CTOs, the real test is whether the technology stack can withstand formal scrutiny once tokenized assets or stablecoins touch any part of the flow. Becoming ‘crypto-native’ isn’t the point.

PSD3 and PSR Make Back‑Office Messes Impossible to Hide

Many financial service providers still treat PSD3 and the proposed Payment Services Regulation as future legal text rather than present‑tense engineering pressure. That misses the operational reality.

The European Commission’s PSD3/PSR package, following the provisional political agreement reached in November 2025, continues to emphasize stronger consumer protection, fraud mitigation, and clearer liability allocation. The most painful effects won’t show up in demos. They’ll land on exception paths that already exhaust teams: disputes, failed authentications, refunds, account‑access errors, and the evidence needed to explain each one.

The pattern looks familiar: chargeback operations scattered across spreadsheets, processor dashboards, and CRM queues. Support sees one slice. Fraud sees another. Product assumes the mess is temporary, but it rarely is.

Once regulators start asking harder questions about customer handling and operational readiness, that scattered workflow becomes a six‑month platform program with no clear owner. Waiting for final wording sounds prudent. Some details do matter. But the low‑regret work is obvious:

- Define dispute ownership across businesses and rails.

- Harden outage behavior around partner APIs.

- Instrument the paths where consumer trust erodes.

- Make fraud rules easier to update with audit history intact.

None of this work is glamorous. It’s the difference between a manageable compliance load and a January full of incident calls.

Minimum Viable Controls Before Launching a New Payment Rail

Minimum Viable Controls for New Rails or Regions

MiCA, PSD3, and the broader fintech sector converge on a practical question: what must be true before you go live on a new payment rail, region, or embedded-finance partner?

A checklist without named owners is a list of good intentions. The table below reflects the floor, not the ceiling. Many institutions discover too late that launch readiness wasn’t a feature problem. It was a control‑plane problem.

| Control | What It Covers | Owner |

| Fraud rule deployment pipeline | Versioned rules, rollback, audit trail, sub‑weekly release cycle | Fraud/Risk Engineering Lead |

| Dispute ownership matrix | Escalation paths, SLA per dispute type, single source of status | VP Engineering or Head of Payments |

| Reconciliation runbook | Ledger‑to‑rail match, exception handling, weekend coverage | Platform Engineering |

| Consent and revocation propagation | Entitlement state, freshness SLAs, downstream cache invalidation | Platform or Identity Lead |

| Sanctions and screening pass | Data completeness checks, explainable decisions, lineage | Compliance Engineering |

| Partner KYC/KYB baseline | Risk segmentation, ongoing monitoring triggers | Head of Platform or Compliance |

| Incident and outage playbook | Rail‑specific runbooks, degraded mode, customer comms templates | Platform Engineering and Support |

Most of these controls look unremarkable on a slide. They’re also the difference between a launch that scales and one that generates a post‑incident review within the quarter.

Real‑Time Payments Raise the Cost of Customer-Visible State Accuracy

The next leap in digital payments comes from the expectations speed creates, not from speed itself.

By the end of 2024, more than 1,000 financial institutions had joined the FedNow Service, with community banks and credit unions accounting for more than 95% of participants. The continued expansion reinforces that real-time payments are becoming operational infrastructure rather than a competitive differentiator. Similar momentum is visible across Asia and Europe.

Customers now expect money movement, notifications, and visible balance changes to align immediately, even if internals still behave like weekday batch operations.

The technical gap can be small. The operational consequences aren’t.

Customers don’t experience a 90-second ledger lag as ‘eventual consistency’. They experience it as the app showing a balance that wasn’t actually settled. Weekend volume, holiday exceptions, and midnight timeouts create a steady tax on on-call teams, reconciliation, and customer experience. Real‑time rails punish vague ownership and sleepy reconciliation habits.

For CTOs, this becomes a capital allocation question: expand rails, or improve reconciliation and customer-visible consistency first? The teams that scale real‑time payments successfully treat reconciliation and dispute traceability as essential infrastructure, not backend chores.

Cross‑Border Modernization Is a Financial Data Integrity Problem

Cross‑border payments are often framed as a standards initiative. In practice, they’re a financial data discipline problem.

ISO 20022 has moved beyond migration planning into operational reality. Ahead of the end of SWIFT’s MT/ISO 20022 coexistence period in November 2025, more than 40% of SWIFT’s daily cross-border payment traffic was already using ISO 20022, with over 1.8 million ISO 20022 payment messages exchanged each day. For engineering teams, the challenge is no longer supporting the standard but preserving richer payment semantics throughout internal systems.

A platform can accept a well‑formed message and still break the process milliseconds later by truncating beneficiary address data into an older schema. That gap shows up directly in sanctions screening, fraud prevention, and explainability, far from an abstract interoperability issue.

Global fintech platforms inherit the customer conversation when cross‑border payments stall and reference IDs disappear. Preserving lineage and screening context across systems becomes a financial‑crime control, not just a data‑engineering best practice.

In an environment of tighter regulatory clarity and heightened scrutiny, traceability is part of the product.

Adaptive Fraud Changes the Release Model, Not Just the Model Score

Fraud detection has entered a more adversarial phase. Generative AI and other forms of artificial intelligence are lowering the cost of convincing phishing, synthetic identity creation, and large‑scale social engineering.

The World Economic Forum’s 2026 Global Cybersecurity Outlook highlights rising sophistication in AI‑enabled cybercrime, with organizations reporting growing concern about AI‑driven fraud tactics.

It’s tempting to respond with more AI. Some of that is necessary. Much of the advantage comes from operational maturity:

- Ship rule changes and threshold updates without waiting for a weekly release train.

- Run predictive analytics with strict controls and reconstruct why a transfer decision was made on a specific day.

- Version fraud rules like production software, with rollback and approval gates.

- Deploy step‑up authentication changes before attacker patterns scale.

AI hype encourages model complexity. The harder, more durable work is tightening the control loop around fraud prevention. That’s where competitive advantage accumulates.

Consent‑Driven Financial Data Flows Become a Platform Primitive

Open banking began as an integration challenge. The shift toward permissioned financial data flows turns it into a control‑plane mandate.

As cross‑business data sharing expands, consent state, entitlement logic, revocation propagation, and freshness SLAs move from plumbing to core product behavior. A revoked consent that lingers in a downstream cache has become a compliance and trust issue, not a minor bug.

Many institutions underestimate the lifecycle complexity of multi‑business data‑sharing obligations across regions and partners. In the U.S., the CFPB’s open banking rule (Section 1033) had its compliance dates stayed amid litigation in 2025. The legal deadline moved, but the underlying entitlement-drift risk didn’t. Entitlement drift accumulates quietly. So does support load when customers see data that should have disappeared.

If permissioned data flows are going to power next‑generation financial products, consent management must be treated as essential infrastructure. That requires identity engineering, platform engineering, and compliance to align on a shared control model.

Embedded Finance Grows Up When the Ledger Gets Harder

Embedded finance has evolved from marketing story to operating reality. The early pitch was simple: add banking, lending, or treasury capabilities to software and unlock new revenue.

As of April 2025, the embedded finance market continues expanding rapidly, projected to reach $7.2 trillion by 2030 according to analyses cited by the World Economic Forum. Growth magnifies the complexity rather than reducing it.

A SaaS company launches cards or lending. Months later, it’s sorting out sanctions alerts, disputes, reserve logic, and partner risk segmentation. Sponsor banks and financial service providers absorb part of the compliance load. Users still blame the platform first.

The durable advantage now comes from ledger design, exception handling, and ownership clarity. Embedded finance stops being a feature the moment cash‑flow reconciliation or capital allocation decisions depend on it.

Digital Wallets Are a Trust and Diagnosis Problem

Digital wallets continue gaining traction because they improve checkout completion and customer experience. They also blur failure paths.

A merchant may see conversion rise after wallet rollout while support volume climbs. Failed transactions can stem from issuer risk, token expiry, device changes, or authentication friction. Without better diagnostics, support scripts devolve into guesswork.

Wallets influence identity continuity, token lifecycle management, and fraud rates. They shape consumer trust at the moment a customer decides whether the system feels competent.

The more interesting 2026 question is which teams can make wallet failures explainable without trapping users in opaque support loops. Clarity under stress is harder to replicate than a polished checkout.

What to Adopt, Plan, and Watch

Across the global fintech landscape, the pattern is consistent. The control‑plane work matters more than feature expansion. Who owns the first step matters more than who sponsors the initiative.

| Trend | Posture | Risk Reduced | Owner |

| MiCA crypto controls | Plan | Licensing, custody, governance gaps | Head of Platform or Compliance Engineering |

| PSD3 and PSR readiness | Plan | Dispute handling and audit failures | VP Engineering or Head of Payments |

| Real‑time payments operations | Adopt | Customer-visible state accuracy, reconciliation drift | Platform Engineering |

| Cross‑border data integrity | Plan | Screening failures and traceability gaps | Payments and Compliance Engineering |

| Adaptive fraud controls | Adopt | Slow rule deployment, weak audit trails | Fraud/Risk Engineering Lead |

| Open finance consent lifecycle | Plan | Stale data and entitlement drift | Platform or Identity Lead |

| Embedded finance ledgering | Adopt | Partner risk and reserve mismatches | Head of Platform or FinOps |

| Digital wallet diagnostics | Watch | Support burden and opaque failures | Payments and Support Engineering |

Prioritize investments that improve reconciliation, state consistency, fraud rule deployment, auditability, dispute ownership, and consent lifecycle management. Plan heavier architectural shifts where market conditions justify them. Watch the noisier narratives, e.g., quantum computing, quantum finance, AI agents.

The Systems That Can Explain Themselves

Finance runs on trust. Trust increasingly runs on explainability.

The platform that wins in the next era of banking and financial services will be the one that can explain itself to a regulator, an auditor, an on-call engineer, and the customer who just watched money disappear from a screen.

Infrastructure debt compounds quietly. So does operational maturity. In 2026, competitive advantage will come from operating platforms that can explain every transaction, every decision, and every exception with confidence.

For many organizations, the remaining challenge isn’t identifying these priorities. It’s executing them while keeping product roadmaps moving. The control-plane work that improves resilience also competes for the same engineering capacity needed to deliver new features.